By Samuel Meringolo, MFA2024

I am sure you have heard about private credit. The asset class that has made headlines, with many even dubbing it the “Golden Age.” But what is this talk all about? Why haven’t many heard of it before? In this higher rate environment, private credit’s floating rate loans have meant higher risk-adjusted returns for the asset class, even temporarily surpassing private equity. This has gotten the attention of many institutional investors who are now adjusting their traditional 60-40 portfolio of public equity and debt respectively and rebuilding it to add alternatives which have proven to offer more resilient and less volatile returns. So, as the asset class grows more so does the opportunities for early-career graduates. In this blog, I will give you a brief overview of this asset class, my academic and professional background prior to joining LBS, my MFA program experience, and lastly my recruiting journey and some advice for those who want to work in private credit.

What is Private Credit?

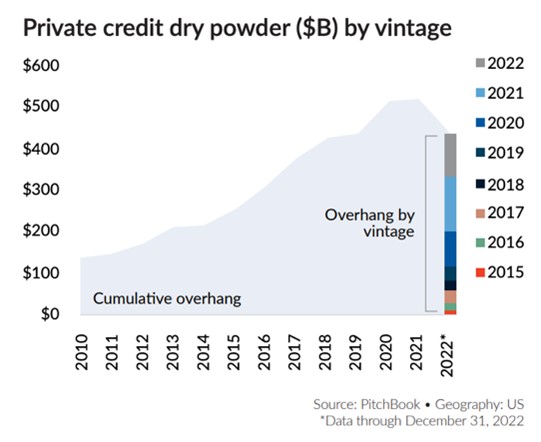

You may often hear about M&A and investment banking, or private equity and venture capital, but the c. $1.7tn private credit asset class, until recently, has not been talked about as much. Private credit, and more specifically, direct lending, is the private non-bank financing of private equity-backed companies. Private credit has usually lent based on a company’s cash flows rather than its asset base, and are often backed by private equity sponsors, although sponsor-less deals also occur. For decades, banks were the main lenders, offering broadly syndicated loans and high-yield bonds. Although lending from these private non-bank financial institutions began over 20 years ago, it was not until the GFC that the demand for private credit began to grow more rapidly as the banking industry faced significant regulations. These regulations included the new Basel regulations which required banks to meet capital requirements set forth by this new risk framework. As a result, the banks were forced to reduce their balance sheets and their risk-weighted assets, which in turn has forced them to de-emphasize the middle-market and become more cautious lenders. This has recently become more apparent, as major banks were forced to syndicate Citrix’s $8.55bn in loans and bonds at a significant discount, resulting in $700m in losses. With that, a major supply demand imbalance became exacerbated, with the supply of private credit capital, which is estimated at c. $400bn in dry powder, being dwarfed by the corporate lending demand. As private credit funds seek to capitalize on this imbalance, there has been more job opportunities in the asset class.

My journey

Now, to give some context on my journey into private credit, it’s important to see where I’ve come from. When I first began my undergraduate degree at ESSEC Business School I knew I wanted to do finance and imagined myself working in a large multinational bank. Every finance student dreams about the day they finally get an offer from an investment bank. Unfortunately, in your undergraduate degree you are not learning much about credit, but instead the basic corporate finance and accounting courses, and a PE course where they talked about LBOs but forgot to give much thought to the “L” (Leverage). So, you don’t usually find credit, credit finds you.

In my case, credit found me. I had my first internship experience at Santander Bank as Credit Risk Analyst. This experience, although a back-office position, gave me a first experience in understanding the importance of diligent credit risk analysis. Following my time at Santander Bank, I was motivated to find another internship, but now in a client-facing front-office position. So, I decided to take a gap year after graduating from ESSEC, to gain two more internship experiences before beginning my master’s degree. As I began applying, I found much more traction with Leveraged Finance internships rather than internships in M&A, as I had a prior experience in credit. In the end, I completed two internships during this gap year. First, a Leveraged Finance position at SMBC, and second, a role in private credit at LFPI, a French investment fund.

For those interested in a career in private credit, it is important to understand the dynamics of the recruitment process. In general, most graduates have future aspirations to work in the buy-side. The buy-side is any investing role that buys and invests in securities for the purpose of money or fund management. This includes roles in private equity, private credit, or in a hedge fund. On the other hand, the sell-side is the selling of securities to the public, such as M&A, equity research, sales & trading, and commercial and corporate banking. Not until recently have buy-side roles been available to early-career graduates. Previously, you had to have done at least two years in the sell-side, and only then would you begin to recruit for a buy-side role. Now, some private equity and private credit roles are opening for summer analyst and full-time analyst positions. This is a meaningful change and has provided many like me the opportunity to work directly in the buy-side without having to work in the sell-side.

My LBS Program Experience

When I applied to LBS, I had already three internships in credit and knew that a post-graduate career in private credit was what I was striving for. So, when reviewing the MFA programme at LBS, I was pleasantly surprised to see some elective credit courses, such as Distressed Investing and Alternative Credit Investing. The programme provides not only those who are interested in credit, but those who are interested in other non-Investment Banking careers to pursue interesting electives. I was also impressed with the number of resources the career services had available. Before even arriving in London, I was able to schedule a one-on-one session with career services, to ensure my CV was strong enough to submit my first applications. Also, the career services have other resources, such as the private credit interview guide that gives a complete overview of what you can expect during credit interviews, and even a buy-side networking event that can help you connect with industry professionals who are actively recruiting.

My Recruitment Process

It was mid-late August as firm’s began posting their summer analyst positions. As the programme began, all you could hear about was which bank had just posted their internship positions, who got the hirevue interview or online tests, and who was getting first interviews. The atmosphere during my first month in the MFA program was very exciting as recruitment was in full swing.

Unlike many of my classmates who were applying to M&A summer internships, I was keen on finding an opportunity in credit. That included Leveraged Finance positions in bulge bracket banks, and private credit positions in investment funds. By mid-September I had submitted 25 applications and was patiently waiting for any updates. By then, I had begun completing my hirevue interviews and painfully long online tests. Finally, in one week I had received multiple responses and had at least two telephone interviews for bulge-brackets and an investment fund. Finally, I was invited to two assessment centres. An assessment centre interview is one day with multiple interviews, which challenge you both qualitatively and quantitively, even requiring you to complete case studies and present them to senior members of the team. After completing these final round interviews, I accepted an offer from Ares Management in their European Direct Lending Origination team. I had worked hard to finally receive an offer from one of the leading players in private credit.

Conclusion

I hope this blog gave you a unique perspective on a career in private credit. It is an exciting time to work in credit and I encourage all those who are interested to do your own research about the asset class and to speak to industry professionals who can provide their first-hand account. Below you may find a few pieces of advice for those interested in a career in private credit:

- Get credit-related experience. Even though you may not be able to get a first internship experience in leveraged finance or private credit, find a position in credit risk or debt advisory. These credit-related experiences will make you a stronger candidate for private credit. To note, as credit internships are less common, an internship in M&A is often acceptable if you are prepared for credit-related interview questions.

- Prepare for credit interviews. Although about 90% of the technical questions will be the same as an M&A interview, it is super important to prepare for qualitative credit questions. For example, “why private credit and not private equity?”, or questions about deal dynamics and why a company is a strong LBO candidate. The Deloitte Private Debt Deal Tracker and other private debt trackers are great resources to follow the sector-specific news and trends.

- Network with credit professionals. Often, smaller boutique credit funds recruit informally. So, networking can be a strong tool to get an informal interview with a credit fund and may be a good option for those seeking their first credit experience.

- Master your financial analysis skills. Working in private credit requires strong accounting and financial analysis skills. Day-to-day, you will be required to understand dense financial due diligence reports and be able to synthesize them to build your LBO model and to redact them in investment committee reports.

Please do not hesitate to reach out to me on LinkedIn, I am happy to speak more about my academic and professional experiences!